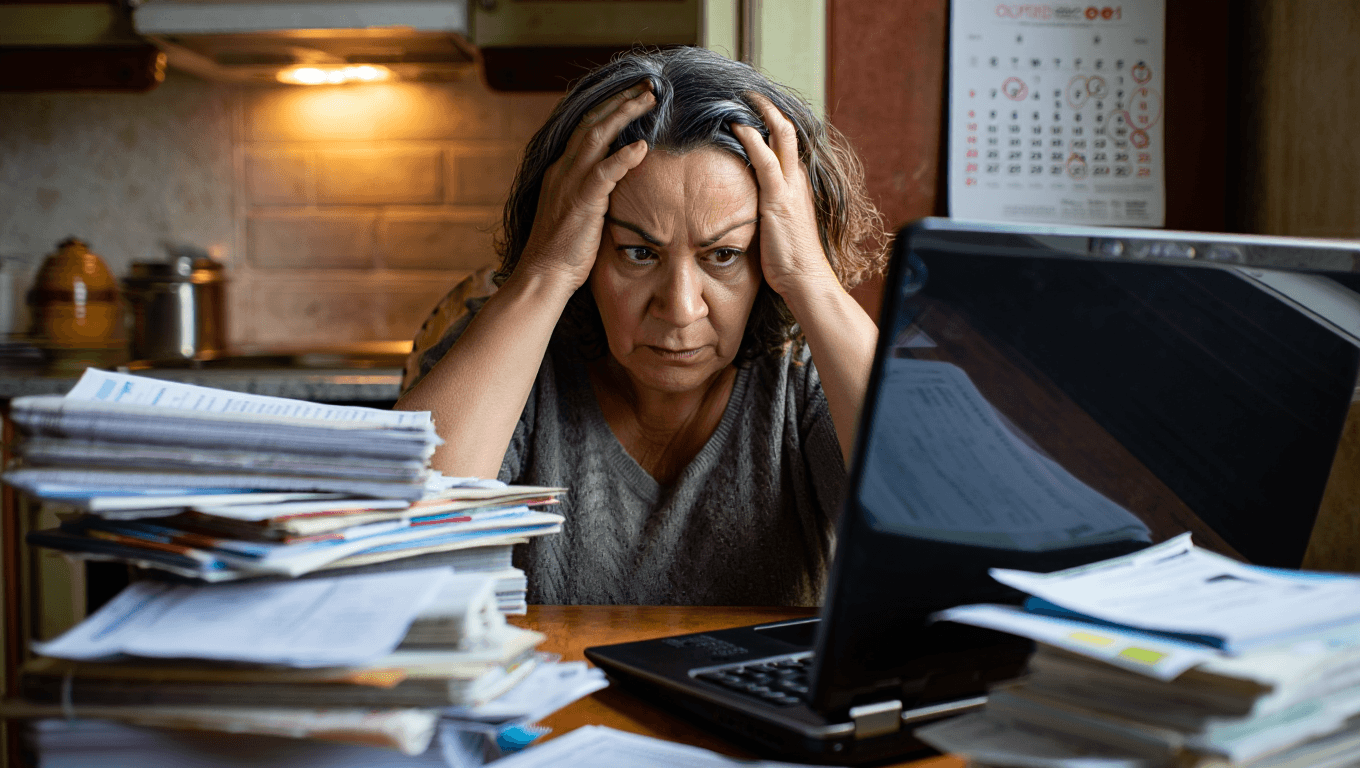

Rising costs and higher borrowing rates have turned routine money choices into real risks for many households in 2024. Small habits — from unused subscriptions to impulse purchases charged on credit — can erode savings and make families vulnerable the moment the economy shifts.

- Everyday purchases can quietly consume hundreds of dollars a year if left unchecked.

- Ongoing fees for gyms and streaming platforms often deliver little value relative to their cost.

- Using credit for nonessential items can create high-cost debt; data show median card rates remain elevated.

- Choosing oversized homes or pricey vehicles increases ongoing bills beyond the monthly payment.

- Failing to save or invest leaves households exposed to job loss, market shocks and rising prices.

Small purchases that become big leaks

It’s easy to dismiss a coffee or a takeout order. But when these purchases repeat weekly, they add up faster than most people expect — often enough to cover a credit-card bill or a month of essentials if redirected. The practical question is whether those expenses belong in your budget or are quietly destabilizing it.

That doesn’t mean cutting every pleasure. For many, the occasional meal out or a streaming night is an important part of wellbeing. The key is planning: decide what matters, set a limit, and monitor it.

Subscription creep and recurring bills

Subscriptions are designed to be painless, and that’s why they’re dangerous. Services you signed up for months or years ago may no longer be useful, but they continue draining the account.

When finances tighten, trimming those recurring charges is one of the least disruptive ways to free up cash. A basic habit: audit automatic payments quarterly and cancel the ones you don’t use.

Credit-card reliance when the rates are high

Charging leisure items or nonurgent purchases can be inexpensive only if you pay your balance in full every month. Otherwise you’re borrowing at rates that often exceed typical investment returns. Research published in mid-2024 found median credit-card APRs remain around the mid-20s, which quickly outpaces most household growth.

Left unchecked, interest compounds. What felt affordable at the time of purchase can become a long-term cost far above the sticker price.

Vehicles: monthly payment ≠ affordability

Many buyers focus on a comfortable monthly auto payment without accounting for insurance, fuel, maintenance and depreciation. Financing a large, luxury or high‑consumption vehicle turns a depreciating purchase into a recurring drain on cash flow.

Practical alternatives include buying a well-maintained used car, choosing models with lower running costs, or delaying an upgrade until you can reduce other debts.

Housing that outpaces your budget

Owning a larger or more expensive home brings predictable extras: higher property taxes, utility bills and maintenance. Those expenses are ongoing and sometimes unpredictable — a roof, heating or plumbing repair can quickly multiply your monthly obligations.

Rule-of-thumb approaches like the 28/36 guideline (no more than 28% of gross income on housing and 36% on total debt) are blunt but useful starting points for assessing whether a property is truly affordable.

When tapping home equity becomes risky

Refinancing or opening a home-equity line gives access to cash but also increases secured debt. Using home equity to plug short-term gaps can leave you paying interest on the very shelter you live in — and may put your home at risk if circumstances change.

The shrinking safety net: low savings rates

Household savings have trended down again: the personal savings rate was reported near 3.6% in April 2024. Many households are effectively living paycheck to paycheck, which means a missed paycheck or unexpected bill can force urgent borrowing.

Planners typically recommend building an emergency buffer of at least three months’ essential expenses. While that goal may feel distant for some, even small, regular contributions improve resilience over time.

Skipping retirement contributions

Retirement accounts are where long-term growth and tax advantages matter most. Not contributing regularly is effectively postponing future security — and it makes achieving a comfortable retirement harder the longer you wait.

If possible, maximize employer matches first, then increase contributions gradually. Time and compound growth are powerful allies; delaying contribution reduces their effect.

Withdrawing retirement money to cover today’s bills

Using retirement savings to erase high-interest debt or cover an emergency can seem rational on paper, but it erases compound growth and often incurs taxes and penalties. Even loans from plans like 401(k)s carry risks: repayment can be difficult, and many never fully replenish the account.

If you must tap retirement funds, treat the decision as debt: create a strict repayment plan and stick to it.

Not having a clear financial plan

Without a simple roadmap — income, fixed costs, savings targets and debt paydown — it’s hard to prioritize decisions. Regularly reviewing bank and card statements, setting measurable goals and revisiting them monthly makes small course corrections possible before problems grow.

- Audit spending monthly to find small leaks.

- Build an emergency fund even if it starts with modest, recurring transfers.

- Pay down high-interest debt first and avoid new consumer debt where possible.

- Prioritize retirement contributions, at least up to any employer match.

The immediate takeaway is practical: review what you spend, protect your savings, and avoid financing lifestyle choices that outstrip your means. Many people can make meaningful progress with small, consistent steps — and that matters more than dramatic, one-off cuts.

My name is Ethan and I am a passionate journalist at Sherburne County Citizen. With a keen eye for celebrity news, I bring you the latest updates and insider scoops on your favorite stars. One of my favorite moments in the newsroom was when we uncovered a wild story about a local politician’s secret rendezvous, shaking up the whole town’s political scene.As a valuable member of the Sherburne County Citizen team, I am dedicated to keeping you informed about major economic trends and providing practical tips for your home. Whether it’s investment advice or DIY hacks, I strive to equip you with everything you need for a successful and fulfilling daily life. Join me on this exciting journey as we uncover stories that shape our community and beyond.